The Trump Effect

Victory Could and Should Lead to a Grand U.S.- China Deal

I hadn’t planned on writing about the U.S. elections, preferring to keep powder dry for post-NPC updates. But with Trump’s victory in the presidential race and Republicans securing both houses of Congress, I’ve taken note. What follows is a collection of my thoughts—not heavy on investment ideas, but hopefully useful for articulating a thesis around China under Trump 2.0.

With Donald Trump returning to the White House, markets are bracing for what could be a transformative era in U.S.-China relations. Trump’s rhetoric on China has historically been fierce, framing the country as both an economic adversary and a threat to American prosperity. His past statements, like “China is raping our country,” painted a clear picture of his stance.

But let’s pause—those quotes are from 2016. What does the president-elect think these days? Here’s a look at his recent remarks:

1. “I had a very strong relationship with [President Xi]. He was actually a really good—I don’t want to say friend—but I got along with him great. He’s a very fierce person.”

2. On potential Chinese action against Taiwan, Trump stated, “I would say if you go into Taiwan I’m sorry to do this, but I will impose a tax of 150% to 200%.”

3. Confident that military intervention would not be necessary to deter a blockade of Taiwan, Trump claimed Xi “respects me, he knows I’m [expletive] crazy.”

4. In a July 2023 Fox News town hall, Trump remarked on President Xi: “Consider President Xi: central casting, a brilliant individual. When I call him brilliant, everyone criticizes… He governs 1.4 billion people with an iron grip. Intelligent, brilliant.”

5. In an October 2024 interview, Trump shared, “I had a robust relationship with him. He was indeed a good—not to imply ‘friend’—but we had a great rapport.”

6. Recently, Trump even said, “I want China to do well, I like President Xi a lot, he’s a friend of mine.”

Does that sound like the rhetoric of a crazed warmonger? Not at all—it sounds like someone keen on making a deal, ready to bring everything to the table.

The Tariff Dilemma: A Stick Leading to a Possible Carrot?

So, what about tariffs? Trump has proposed a 60% levy on Chinese imports and 10% on goods from other countries. Specific to Chinese automakers, he’s stated, “They’re going to pay a 100 per cent or maybe even a 200 per cent tariff because we’re not going to let them come into our country and destroy what’s left of our auto industry.” It’s clearly a “stick.” But once you start talking percentages, you enter the realm of dealmaking.

This leads to my thesis: while these measures are designed to pressure China, the end goal could be strategic—a broad, new accord between the United States and China. GaveKal has suggested something like a “Mar-a-Lago Accord,” inspired by the 1985 Plaza Accord, in which major economies coordinated to adjust currency values and address trade imbalances. This new accord might include a controlled appreciation of the Chinese yuan against the U.S. dollar, rebalancing economic dynamics between the two nations. For context, the Plaza Accord led to a significant yen revaluation that never returned to pre-Plaza levels.

(Yen/USD rates, lower means yen is more expensive)

Trump’s prior administration set a precedent with moves to “punish” China, from targeting intellectual property theft to using tariffs as leverage. His methods raised concerns among economists and industry leaders, but the objective was clear: create leverage.

Despite the imposition of tariffs, the U.S. trade deficit widened, increasing by 13.15% in 2022 to $971.12 billion. This trend suggests that tariffs didn’t effectively reduce the trade imbalance. Instead, they reshuffled trade relationships, with imports being redirected through other countries, keeping the deficit intact.

Yet, by establishing a framework of power dynamics, Trump’s actions could position the U.S. for a more favorable negotiating stance. With the potential for a “Mar-a-Lago Accord” on the horizon, we could see a trade deal that addresses economic imbalances.

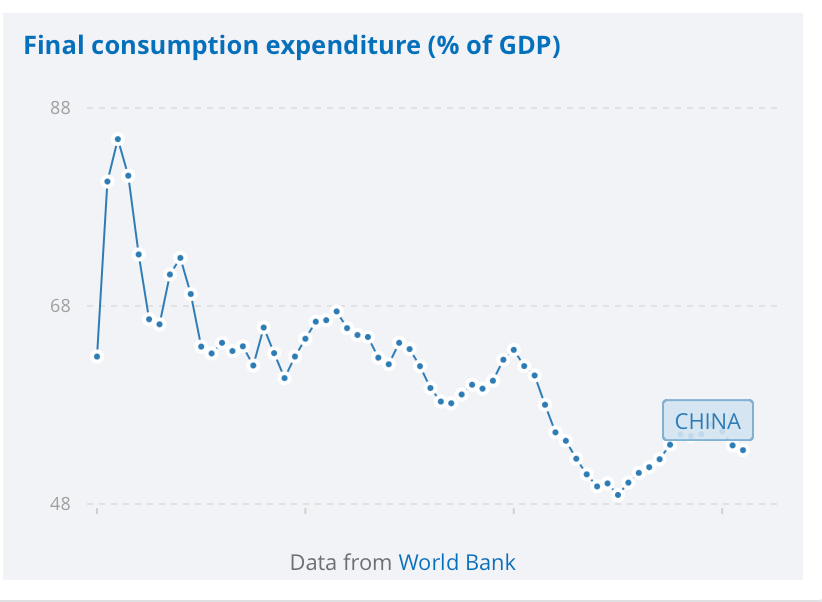

For the U.S., reshoring efforts remain a priority, especially after pandemic-induced supply chain disruptions. Such a deal could incentivize companies to bring manufacturing back home, creating jobs and making supply chains more resilient. For China, an agreement could support its transition to a consumption-driven economy rather than an export-reliant one, aligning with long-term goals. A mutually beneficial accord could encourage China to focus on its internal demand, helping it evolve its economic model.

In this way, both countries could benefit: the U.S. could strengthen its manufacturing base, while China could rebalance towards internal demand. Chinese policymakers increasingly recognize the value of domestic consumption, and a deal that supports this would be welcome. A revalued RMB, while making exports less competitive, could still offer a net positive, especially considering that protectionism has eroded currency advantages anyway.

There is a growing understanding of the value of internal demand now in the upper echelons of Chinese economic policy making, and a bargain that helps achieve that will be acceptable, Now clearly this will significantly revalue RMB-denominated assets, while making Chinese exports less competitive, and this is the slack that needs picking up by domestic demand.

(Compare the Nikkei Chart to that of the JPY earlier, Accord fuelled a massive equity boom, on top of Japanese Assets bering revalued in USD terms).

Another factor they might consider is that protectionism is eroding currency advantages anyway, so the net impact of such a revaluation of the RMB won’t be as negative as claimed. In fact accounting for capital flow reversal, it could potentially be a net positive.

While scepticism is understandable, the end result of Trump’s strong-arm tactics could lead to a redefined, balanced relationship between the world’s two largest economies. By addressing these imbalances, a potential Mar-a-Lago Accord could set the stage for sustained economic stability, benefitting both sides.

Ultimately, if Trump uses his leverage wisely, we could see this shift in U.S.-China relations as a stabilizing force rather than a destabilizing one. The U.S. and China may finally find a way to coexist in a way that mutually strengthens each economy. It’s a tall order, but a grand deal could just be the legacy Trump’s administration leaves behind in this complex global relationship.